Gold as a hedge or safe haven.

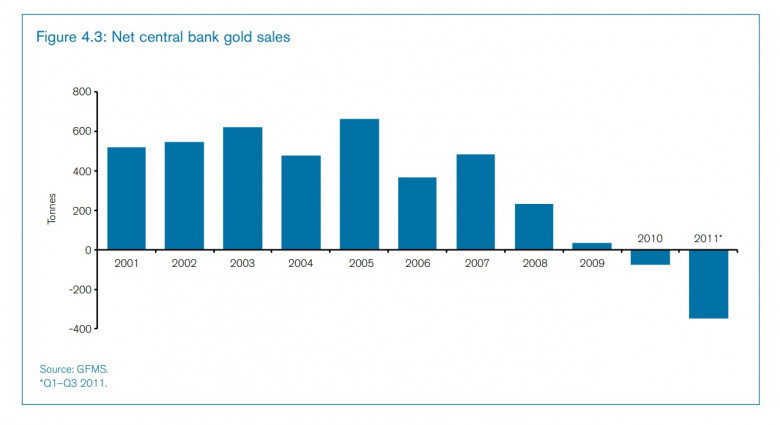

The Taskforce likewise inspected the job of gold as a fence or on the other hand a place of refuge. Albeit gold has no conventional situation in the worldwide financial framework today, it regardless keeps on assuming a significant part, comprising around 12% of worldwide stores. Lately, that rate has been rising, not just in light of the fact that the price of gold has expanded, yet in addition, since national banks have become net purchasers, as opposed to net dealers, of bullion.

This pattern went on in 2011, as the Figure shows. By far most of this movement has been by the national banks of emerging nations, which have customarily held close to nothing or on the other hand, no gold in their unfamiliar trade saves. In any case, the worldwide load of gold held as stores by national banks (about $1.4trn, barring the IMF and the Bank for Global Settlements as of Q3 2011) is simply a small portion (even at current costs) of the present worldwide stock of cash. As indicated by ongoing cash supply (M2) information (for example cash and stores) delivered by the Government Hold, a load of cash in the US alone sums about $9.7trn, or multiple times the worldwide stock of gold stores.

It is a long way from clear what extent of gold is ideal in a national bank's saves portfolio, as it will rely upon various variables: the size of the stores and their sufficiency for day-to-day needs; whether the nation is a gold maker; the national bank's gamble resilience, trust in government-issued types of money and its perspectives on future cost developments. Nonetheless, an agreement is by all accounts arising among the recently resource-rich nations that having some bullion ought to progressively turn into a vital piece of their long haul technique. Without a doubt, resource-rich national banks that have been purchasing gold consider it to be a valuable method for enhancing their property, diminishing their openness to US dollars, and safeguarding themselves against tail gambles - genuinely awful results, for example, hyper-expansion or sovereign default - yet there are different reasons too.

The customary perspective on gold as an extreme resource actually conveys the weight and there is no default risk in holding gold. A vital disadvantage of gold is that it creates no interest return, however on the off chance that effectively utilized, gold stores can create positive returns in a rising business sector. To be sure, various national banks looking for higher returns have taken part in gold loaning, gold trades, and collateralized acquiring.

In a couple of years, there has been a substantial change in the way of behaving of national banks with regards to making due their stores. As of now, as verified over, the dollar is still the essential save money, with the euro, the yen, and the pound all thought to be less appealing choices, and the renminbi still to accomplish full convertibility. Be that as it may, a persevering disappointment with the capacity of the dollar to keep up with its worth has prompted some enhancement.

In the past ten years, there has been a gigantic aggregation in unfamiliar trade saves, which has matched with a sensational change yet to be determined held by created and emerging nations. While in 2000 stores held by created economies ($1.2trn) were practically twofold those of developing business sector economies ($0.7trn), by the first quarter of 2010 the opposite had become valid, with the last option having amassed $5.5trn, contrasted and only $2.8trn in the created world. From that point forward, as